Madagascar Vanilla - Market report n°03 - April 2025

The downward correction of the vanilla market in Madagascar was inevitable, but it was its avoidance that surprised us, and its duration may surprise us again.

On the one hand, decisions from 2020 to 2023 slowed down exports with limitations on dates, prices and approvals, and caused stocks to build up, with prices collapsing more rapidly and extremely as a result. On the other hand, to compensate for this loss of price and income, vanilla farmers have accelerated mass planting to recover on the volume effect, all crowned by a twist of fate signed “Mother Nature” with a record flowering for 2025.

Together, these three effects have already created and will continue to create “potentially dramatic” conditions for an origin which alone produces far more vanilla than the world market consumes. This situation of greater supply than elastic demand ushers in a period of low prices.

The 2023 campaign is a good illustration of a market losing its bearings, a victim of regulatory instability, with 4,300 tonnes exported in 7 months, just after the liberalization of prices, to secure at least 2 years of consumption outside Madagascar in one go, far from the turmoil.

Although rational decisions to return to low prices for some, and speculative positions for others, are at the root of this unusual craze. It's the fact of quickly hedging long in short period and beyond actual needs for the wrong reasons, driven by fear of sudden change in export regulations, which is upsetting the balance of the sector and the regular buying habits of players traumatized by 4 years of fixed export prices at 250 USD, with consequences for several campaigns.

Production : uncontrollable overproduction worsens

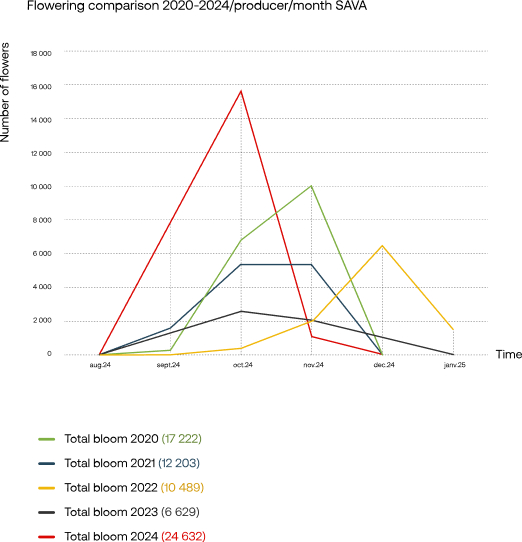

- Based on our flowering studies, we estimate a record production, at least 2,5 times higher than normal, for 2025.

- Information about a “sharp” drop in production for 2024, exacerbated by the damage to vanilla caused by cyclone Gamane, proved to be misleading, midway through the 2024 campaign. The drop is real, but it is limited to certain coastal zones and has been partially offset by a good preparation yield, good production in intermediate and mountainous zones, and an increase in the number of plantings combined with a drop in orders from covered buyers.

- 95% of flowers were fertilized in just two months, including 32% in September and 63% in October (peak), which means that 2025 production will mature earlier than usual. We estimate that the majority of pods will reach maturity between the end of April to mid-June 2025, and for the first time, the SAVA and DIANA regions will open at the same time. For 2025, a large quantity of new vanilla will arrive on the market at the same time, as early as May 2025.

- The hope that prices will rise again between now and the close of exports at the end of June 2025, as they did at the end of the previous campaign, means that farmers, unaware of the imbalance, are waiting to sell their “dormant” lots and are unintentionally contributing to the build-up of stocks. It is possible that some farmers will have 2 or even 3 campaigns in hand at the start of the 2025 campaign. These will overlap and accumulate with all the other vanilla leftovers not sold in the 6 major producing regions.

- Although the aim of setting a floor price is to protect producers against price volatility and guarantee a minimum income, it will have a number of perverse effects, including reduced competitiveness and, above all, the creation of overproduction through the build-up of stocks that we are currently experiencing.

Quality : getting better and better

- For 2024, in a declining market with cumulative overproduction, the pressure to harvest early is low, resulting in mature pods and a direct increase in quality... and quantity... We are, however, seeing more humid vanillas, with some farmers and collectors returning to vacuum-packing vanillas that have not been properly dried. This is a “speculative” consequence of the feeling that production is in short supply, and of the short-term hope that prices and demand for gourmet vanilla will rise, and that vanillas, even wet ones, will be snapped up. They, too, are victims of a misjudgment about the sharp drop in production.

- For 2025, with flowers fertilized in just 2 months as against the usual 4, the majority of pods will, for once, reach maturity at almost the same time. This will result in very fine, homogeneous 2025 qualities, with vanillin levels easily exceeding 1.8% for the long varieties.

- With the enormous flowering, there is a risk of over-pollination, with a possible increase in the share of vanilla cuts by 2025. Nevertheless, our recent visits to the plots have alleviated this fear, with a crop that is growing well, with long pods and a normal coulure rate. To be continued...

- With 66 nicotine analyzes carried out by Eurofins France over 2 years on all types of vanilla samples (Green-Wet-Dry-Prepared) and separating smokers and non-smokers, we can state with certainty that nicotine contamination is caused externally by chewing tobacco smokers, in particular those who do not respect the hygiene of handwashing during the handling and preparation of their vanilla after smoking. 100% of the samples from the smokers' group had higher nicotine levels than those from non-smokers, while 100% of the green vanilla samples analyzed showed no trace of nicotine. An awareness-raising campaign is needed among smokers to resolve the nicotine issue.

Prices : dropping ?

- A long market covered, 2022 and 2023 leftovers still available despite 4,300 tonnes exported in 7 months, 2024 production much higher than forecast, 2025 production to come up sharply, and yet... export barriers will further slow down sales and will mechanically translate into a drop in local vanilla prices. In 6 months, since the opening, local prices have already fallen by over 50%. Our fear is that the situation will worsen from May 2025 onwards, when the accumulated residues will overlap with the new campaign.

- Two markets stand out today. On the one hand, the conventional market (80%), which is freer for producers and collectors, but whose local prices are set by the balance between supply and demand, and on the other, the certified market (20%), which is more demanding on producers in terms of traceability, hygiene and documentation, but more protective thanks to the minimum prices guaranteed by certification : Bio, Fairtrade or Rainforest Alliance. Forcing the entire conventional market to become certified is utopian today, given the lack of demand.

- However, a return to FOB export prices of 15-20 USD/kg, as was the case 15 years ago, “seems” unrealistic to us today, given the sharp rise in exporters' fixed costs due to inflation, rising logistical, production and certification costs, and above all a new dynamic of demand that is more concerned with the well-being of producers at source, with gaps to fill in terms of living wage and living income. Food prices rose by an average of 208% between 2013 and 2025, with the price of rice at 340 ar/kapoaka (local unit) in 2013 compared with 900 ar/kapoaka in 2025, i.e. +165%.

Sustainability : a small step forward

- In 2024, 17% of approved exporters (21 out of 123 exporters) joined the 24 importers in the SVI (Sustainable Vanilla Initiative: http://www.sustainablevanilla.org/) to “create the conditions for a sustainable vanilla industry”. On paper, this is a very good initiative, necessary for the industry. But to succeed on the ground, it will need, in “our opinion”, more members, more listening and less temptation to over-regulate and control a market already short of sales. In the current context, where it is the imbalance between supply and demand that is dragging prices down (and no exporter), with stricter regulations on imported deforestation and human rights, alleviating the shock with a sustainable response is welcome.

- Diversification into other cash crops (cloves, coffee and cocoa) in addition to vanilla is seen as one response by resilient producers to extreme price volatility. Very little abandoning of vanilla.

- Proposals to give back part of the 3-year USD 4/kg CNV fund to farmers with the construction of schools, basic health centers and wells in remote rural production areas. One infrastructure per year per exporter participating in the funds would be a major step towards greater sustainability and accountability and would demonstrate good governance of the sector.

n conclusion, Madagascar has confirmed its dominant position on the market and has everything to consolidate it, with sustainability underway, Bourbon origin, exceptional quality, a structured and certified industry, existing CSR policies, thousands of hectares of plantations, vanilla available everywhere, endemic biodiversity, involved governance with the MIC (Ministry of Industrialization and Trade) and the Caisse Nationale de Vanille (CNV), expert producers in planting and preparation, and exporters who are “already” professional, but not supportive.

Madagascar, with its accumulated surplus stocks, its creation of an underestimated and uncontrollable overproduction and its falling prices, has few alternatives left but to stimulate, facilitate and free up exports, and to let market forces rebalance themselves by urgently removing the closing date and price barriers that didn't exist before, or in competing producing countries, to stop accumulating surplus stocks year after year, the source of all our ills.

Closing a campaign or reducing exporters approvals when supply is abundant and demand is not infinitely expandable, compromises the next campaigns, and puts the whole industry in danger and brings its operators to their knees, both financially and psychologically.

The only way for prices to rise again is for the market to reverse, with demand for vanilla outstripping supply, as was the case from 2015 to 2020. With free and competitive prices, demand will naturally increase; while supply will fall because of these same free prices, which will finally discourage overproduction by producers. A natural reversal of the imbalance may take a few years, but the recent situation of the natural gap of cocoa and coffee leaves us optimistic.

Difficult choices to be made, high stakes, words measured out, to translate the current market situation as seriously as possible.

Of course, this “technical” analysis is based on “our own” perceptions, projections and market data at a given moment. As the industry is in a perpetual state of motion, today's truth may be obsolete tomorrow.